Amarin: How Cost Cutting Affects Cash Burn And Profitability

BOOKMARK / READ LATER

Disclosure: I am long AMRN.

Amarin (AMRN) has slashed expenses in an attempt to shorten the path to profitability without approval for Vascepa's ANCHOR indication, although Amarin also mentioned that they are still vigorously pursuing the ANCHOR indication. In this article, we are going to look at the anticipated cost reductions for Amarin going forward based on its 10-Q and earnings call comments.

Effect Of Cost Reductions

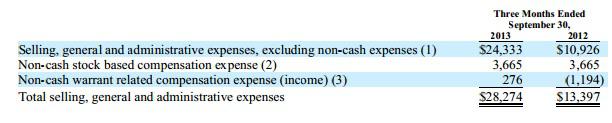

Amarin reduced its workforce by 50% and mentioned that it expected SG&A to have a somewhat similar reduction. SG&A expense was $28.3 million in Q3, but some of that was non-cash based expenses. We can assume that cash expenses for SG&A will be reduced to approximately $13 million per quarter or $52 million per year going forward.

(Click to enlarge)

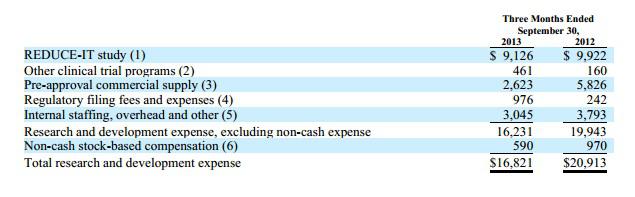

As for R&D expense, the majority of that $16.8 million expense in Q3 came from non-staffing related items. The other clinical trial programs line relates to AMR102. Further development of that product may be discontinued if Vascepa does not receive approval for its ANCHOR indication. The pre-approval commercial supply expense should go down in the future since that relates to purchases of Vascepa API received and expensed before regulatory approval for that supplier. Once regulatory approval is received, future purchases are treated as inventory.

Therefore, we are estimated cash R&D expenses to be $12 million per quarter or $48 million per year going forward. This may decrease to around $2.5 million per quarter or $10 million per year if Amarin decides to stop the REDUCE-IT and AMR102 studies.

(Click to enlarge)

Total Cash Outflows

Here's a look at the total estimated cash expenses and required payments in each year. This does not incorporate the revenues and COGS associated with Vascepa sales. With REDUCE-IT, Amarin is looking at around $131.7 million in cash payments in 2014, increasing to $160.2 million in 2016 for a three year total of $435.1 million.

With REDUCE-IT

$ Million

|

2014

|

2015

|

2016

|

SG&A

|

$52.0

|

$52.0

|

$52.0

|

R&D

|

$48.0

|

$48.0

|

$48.0

|

BioPharma

|

$26.5

|

$38.0

|

$55.0

|

Cash Interest

|

$5.2

|

$5.2

|

$5.2

|

Total

|

$131.7

|

$143.2

|

$160.2

|

Without REDUCE-IT, Amarin is looking at around $93.7 million in cash payments in 2014, increasing to $122.2 million in 2016 for a three year total of $321.1 million.

Without REDUCE-IT

$ Million

|

2014

|

2015

|

2016

|

SG&A

|

$52.0

|

$52.0

|

$52.0

|

R&D

|

$10.0

|

$10.0

|

$10.0

|

BioPharma

|

$26.5

|

$38.0

|

$55.0

|

Cash Interest

|

$5.2

|

$5.2

|

$5.2

|

Total

|

$93.7

|

$105.2

|

$122.2

|

Amarin mentioned in the earnings call that it expected to use less than $80 million cash for operations in 2014. One thing that is uncertain though is how much of the BioPharma payments are classified under operating or financing activities. Most of the payments in 2014 are interest-related as the 10-Q states that quarterly payments do not begin to reduce the principal balance until Q4 2014. Amarin appears to be guiding towards at least $43.7 million (if the last payment is 100% classified under financing activities, although it is more likely to be only partially classified under financing activities if it is at all) to over $51.7 million (if all payments are classified under operating activities) in gross margin for 2014.

Sales Expectations

It appears that sales growth has stalled out as Amarin adjusts its sales force and attempts to rebuild as a smaller company. Vascepa prescriptions during the week ending November 2 (first full week after the layoff announcement) reached 6,234 vs. 6,255 for the week ending October 4, while NRx declined to 2,986 for the week ending November 2 from 3,078 during the week ending October 4. Sales growth may be stagnant for a while as Amarin adjusts, but Vascepa will need to demonstrate growth again fairly soon if prescriptions are to reach the levels needed for Amarin to be worth $3 to $4 per share without ANCHOR approval. We will probably give Vascepa until January to show new prescription growth again before becoming more concerned.

Average revenue per prescription has been lower than expected, so we are going to use $125 per prescription (prescription numbers based on Symphony data). At 68% gross margin, this would translate into $85 in gross margin per prescription. For Amarin to reach $51.7 in gross margin in 2014, would require 608,000 prescriptions during 2014. To reach that level would require NRx growth of approximately 90 per week throughout 2014 assuming that Vascepa enters 2014 at 3,000 NRx per week.

2016 cash flow break even numbers will be achieved at around 1.22 million prescriptions without REDUCE-IT and 1.6 million prescriptions with REDUCE-IT assuming that gross margin reaches 80% then.

Continuing REDUCE-IT

During the Q3 earnings call, Amarin's management mentioned that it would need to make a "serious determination as to whether funding the continuation of the REDUCE-IT trial is feasible" if it does not get approval for the ANCHOR indication. Although the REDUCE-IT study represents a very significant expense for Amarin (estimated at 27% of 2014 expenditures), we feel that the value of the study makes continuing it a priority for Amarin if at all possible.

The ADCOM panel's vote against Vascepa's expansion for its ANCHOR indication combined with the retraction of the ANCHOR study Special Protocol Assessment agreement resulted in the reduction of Amarin's market capitalization by nearly $1 billion. A successful REDUCE-IT study that results in label expansion would figure to increase Amarin's value by at least that much. Spending $100 million for a chance to raise market capitalization by over $1 billion (even 3-4 years down the line) seems like a reasonable risk if it can spare the funds for study completion.

Conclusion

Amarin has cut expenses significantly and positioned itself to reach cash-flow break even with significantly fewer prescriptions than before. However, there is still a lot of uncertainty about what Amarin will do with REDUCE-IT and whether it can regain Vascepa sales growth with its smaller sales force. We are going to assume that the December 20 decision will be negative for the ANCHOR indication and will closely monitor the sales growth issue.

No comments:

Post a Comment