Long Position Open at 3.05

Volatility Stop Bearish

Volatility Stop Bearish

Low Range 2.881 (February 4 of 2014)

High Range 6.67 (September 19 of 2013)

Business Gap Bridget 56.82%

High Range 6.67 (September 19 of 2013)

Business Gap Bridget 56.82%

33% of The Planned Profit on Business Gap 18.75%

50% of The Planned Profit on Business Gap 28.41%

Low Margin Requirement 25%,...Low exposure of Capital

Support Level at 4.02

Self-Correction Level at 4.78

Self-Correction Level at 4.78

Resistance Level at 5.53

Trend Performance "Downtrend"

Bollinger Band Alert Trading "Neutral"

Average Price Paid Must be -Below-For a Long Position at 3.48 oK!!!!

Average Price Paid 3.05

Average Price Paid 3.05

Cash Marginable Securities $ 250,000.00

Non-Marginable Securities $ 1,000,000.00

Scaling Rate 0.33 Cents

Scaling System Up and Down Scaling Amount on each level $ 100,000.00

The market has experienced a sharp pullback in January and this has created ideal conditions for short sellers. As most investors know, stocks often sell way above "fair value" when investors are excited and when shorts gets squeezed. By contrast, stocks also often get pushed down far below reasonable levels when margin calls hit longs and when shorts pile on to exacerbate the selling. When a perfect storm hits with a sharp market correction, margin call selling, and shorts going overboard (in some cases), it can cause a stock to get crushed and many shareholders often capitulate. When this happens, it can be a great opportunity for contrarian investors to strike.

Buying beaten-down stocks that get even more pummeled by shorts in a market correction can be very rewarding. For example, in late 2012, shares of Hewlett Packard (HPQ) were pushed down to ridiculous levels of just around $11. Well known shorts like Jim Chanos were spotlighted by the media for having shorted this tech giant, other shorts piled in, and many investors capitulated even though the company was expected to post profits in the coming years. Hewlett Packard shares ended up nearly tripling in value from the lows of about $11, and contrarian investors who could see past the negativity made huge gains.

A similar opportunity appears to have arisen with Forest Oil (FST) as it has dropped sharply in recent weeks. It is heavily shorted and it is also very oversold with a relative strength index of less than 30. Just take a look at the chart below to see the pain endured by longs in recent weeks and months:

(click to enlarge)

For a number of reasons, it could potentially pay off big to be contrarian and buy shares of Forest Oil at current levels. No, this company does not have the financial strength of some major oil companies, (it has plenty of debt), it is not growing as fast as many smaller oil companies, and so forth. However, at some point, fearful longs are potentially selling too cheap, and shorts are getting overly confident and complacent with this stock, just as many did with Hewlett Packard about a year ago. At the end of the day, shorts could be right in believing that this is not the best oil company in terms of balance sheet strength or production growth. However, that does not mean it is not a screaming buy at current levels. In the past few weeks this company has seen a downgrade by analysts at RW Baird, but even that bearish downgrade has set a $4 price targetwhich would give investors upside of roughly 33%.

More recently, on January 23, analysts at Moodys affirmed Forest Oil's B2 debt rating with a negative outlook. Moodys stated:

"The completion of a series of major divestitures has left behind a much smaller E&P company seeking to stabilize its operations, generate higher quality cash flows and ultimately achieve a reduction in debt leverage," commented Andrew Brooks, Moody's Vice President. " The negative outlook remains in place reflecting the execution challenges Forest faces in achieving these objectives following its significant downsizing.

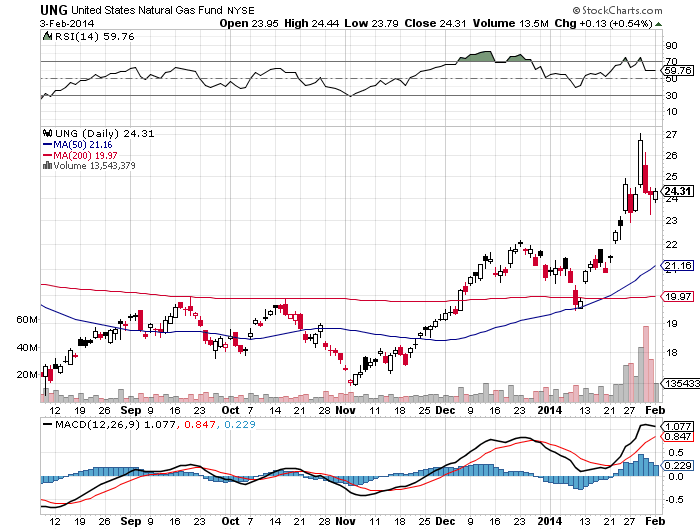

Now I have to wonder if anyone is surprised with the "negative outlook" since every investor can clearly see that Forest Oil has about $1.6 billion in debt. This debt load is a potential downside risk to consider if oil and natural gas prices were to plunge. However, oil prices are strong at nearly $100 per barrel and natural gas prices have been surging recently. Just take a look at the chart below to see the major spike in natural gas prices in the past several days. While it is hard to say if prices will remain this high on a sustained basis, it is certainly going in the right direction for Forest Oil. With oil and gas prices strong and rising, the balance sheet becomes less of an issue and that could eventually pose a problem for shorts. It appears that shorts have become carried away and this complacency could lead to a significant short covering rally.

(click to enlarge)

We see that one analyst above has set a $4 price target for this stock. Now let's take a look at analyst earnings estimates. The consensus estimates for 2013 are for profits of 18 cents for 2013. However, profits are expected to jump to 42 cents in 2014 and to 65 cents in 2015. That means this stock is trading for around 7 times 2014 earnings which is very cheap. This is another reason why shorts might have gone too far on this stock. With profits expected to rise significantly this year, the concerns over leverage are greatly diminished. The consensus estimates for 2014 are the collective work of 10 different analysts which should increase investor confidence. Furthermore, there is a very good reason as to why earnings should jump for this company in 2014. Forest Oil is planning to increase its drilling budget in 2014 and oil production is expected to jump from about 3,465 bopd in 2013, to around 6,800 bopd in 2014. This represents a nearly 100% gain in oil production which is sure to lead to higher revenues and profit margins. This increase in oil production is possible because (not too long ago) the company acquired assets in the oil rich Eagle Ford range. This will give it the ability to produce more oil in 2014.

According to Shortsqueeze.com, nearly 21 million shares (which is equivalent to about 24% of the float), have been sold short. The shorts appear focused on the less than robust earnings in 2013, which have been due to weak natural gas prices and not enough exposure to oil. However, the company is clearly shifting production to oil in 2014 and that should begin to dramatically improve financial results in the coming quarters.

After a significant market pullback, there are many stocks to consider buying. However, when markets rebound, stocks that are low-priced (below $5), very oversold, and heavily shorted often see the biggest rebounds. In a strong rebound, this stock might be able to head back towards the 50-day moving average which is $3.70 per share. That would possibly give investors quick gains of about 20%, and it appears to have even more longer-term upside as earnings growth thanks to the shift to oil kick-in. For another cheap oil sector stock that could rebound sharply, read this article which details my top below $5 pick for 2014.

Here are some key points for Forest Oil:

Current share price: $2.88

The 52 week range is $2.88 to $7.24

Earnings estimates for 2013: 18 cents per share

Earnings estimates for 2014: 42 cents per share

Annual dividend: none

Current share price: $2.88

The 52 week range is $2.88 to $7.24

Earnings estimates for 2013: 18 cents per share

Earnings estimates for 2014: 42 cents per share

Annual dividend: none

Data is sourced from Yahoo Finance. No guarantees or representations

are made. Hawkinvest is not a registered investment advisor and does

not provide specific investment advice. The information is for

informational purposes only. You should always consult a financial

advisor.

are made. Hawkinvest is not a registered investment advisor and does

not provide specific investment advice. The information is for

informational purposes only. You should always consult a financial

advisor.

No comments:

Post a Comment